Russia’s automotive industry: looking under the hood

The major factors underlying the recent market dynamics are rapid income growth, increased availability of consumer credit, low per capita ownership rates and an ageing car fleet. As these factors will persist in Russia for years to come, the potential for further market growth will remain. Unlike the booming domestic market, Russia’s car exports remains relatively staid at around 130,000 vehicles annually.

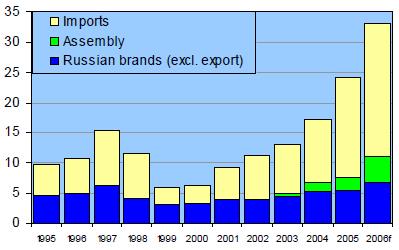

A prominent feature of market expansion in Russia is that it has been driven primarily by import growth; domestic model production volumes have decreased steadily from 1,022,000 units in 2000 to 911,000 in 2005. Despite a 30% average annual growth rate in imports, domestic carmaker AutoVAZ has retained its dominance in the market with annual production of more than 700,000 units. However, as rising domestic costs and rouble appreciation erode the price competitiveness of domestic models, Russian carmakers must focus on quality enhancement by looking to possible alliances with foreign manufacturers or other ways to access innovative technologies. For example, the GAZ group this year acquired a British light commercial vehicle manufacturer, as well as US automotive plant of DaimlerChrysler and its production licenses. Moreover, the ubiquitous Volga will be redesigned to maintain current production volumes rather than phased out.

Humble charm of industrial assembly

In April 2005, the Russian government proposed an “industrial assembly” regime to promote foreign carmakers to set up assembly plants in Russia and bring in original equipment manufacturers (OEMs). Under the regime, a declared amount of auto components can be imported at either zero or 3-5% import tariffs. To receive the dispensation, OEMs are required to organize production of at least 25,000 units a year on Russian soil and reduce imports of components by 30% within 7-8 years. As of October 2006, nine investment agreements had been concluded with foreign OEMs on construction of greenfield plants in Russia (Toyota, Nissan, GM, Volkswagen and Ford) or joint ventures (Autoframos-Renault, GM-AutoVAZ) and Russian-owned companies (Izh-auto, Severstal-auto), which have already begun assembly of South Korean Kia and SsangYong models at existing production sites.

The total number of foreign vehicles assembled in Russia in 2010 should reach around 600,000 units, a four-fold increase from the 2005 level. Despite this impressive projection, foreign OEMs face numerous challenges as they enter the Russian market. The average capacity of their Russian assembly plants will be held to a suboptimal level of 50,000 units, which is quite small compared to similar plants in Eastern Europe (average capacity 230,000 units). Moreover, no international suppliers have plans for massive expansions into Russia. Given the humble OEM capacity plans, it comes as no surprise that foreign auto component manufacturers will concentrate mainly on producing car parts for the Russian after-sales market.

Auto components make a crucial difference

Russia’s automotive industry remains highly vertically integrated, with domestic manufacturers producing up to 60% of their components in-house. Thus, despite a relatively high volume of car production, there are currently very few independent auto component manufacturers in Russia. This is especially striking when compared with the recent rise of the auto component sector in Eastern Europe and China. Several large auto component suppliers have emerged as OEM spinoffs, but domestic production is still highly concentrated within carmakers. Russian manufacturers have a strong position in the component market for domestic models where they possess competitive advantages in price, location and customer relations, but the majority of them still fail to produce innovative products or meet required quality levels.

In our opinion, “industrial assembly” should be viewed as necessary but not sufficient tool of government automotive policy. The crucial task for the industrial policy in Russia now is to propose effective measures for stimulating production of modern auto components as well as emphasize domestic R&D and import of technologies.

Structure of Russia’s domestic car sales in 1995-2006, USD billion

Source: ICSS